See This Report on Mortgage Investment Corporation

Table of ContentsMortgage Investment Corporation Can Be Fun For AnyoneGetting The Mortgage Investment Corporation To WorkMortgage Investment Corporation Can Be Fun For EveryoneFacts About Mortgage Investment Corporation RevealedRumored Buzz on Mortgage Investment CorporationNot known Facts About Mortgage Investment Corporation

After the lender markets the financing to a home mortgage investor, the lending institution can utilize the funds it receives to make more financings. Besides offering the funds for lenders to produce more finances, capitalists are essential due to the fact that they set standards that contribute in what kinds of financings you can get.As homeowners pay off their mortgages, the settlements are gathered and dispersed to the exclusive capitalists who bought the mortgage-backed protections. Since the financiers aren't secured, conforming financings have more stringent guidelines for figuring out whether a customer qualifies or not.

Capitalists also handle them in a different way. Rather, they're marketed straight from loan providers to private investors, without including a government-sponsored business.

These firms will package the fundings and market them to personal capitalists on the secondary market. After you close the finance, your lending institution may sell your lending to a capitalist, yet this generally does not change anything for you. You would certainly still pay to the lending institution, or to the home mortgage servicer that handles your home mortgage payments.

The Best Guide To Mortgage Investment Corporation

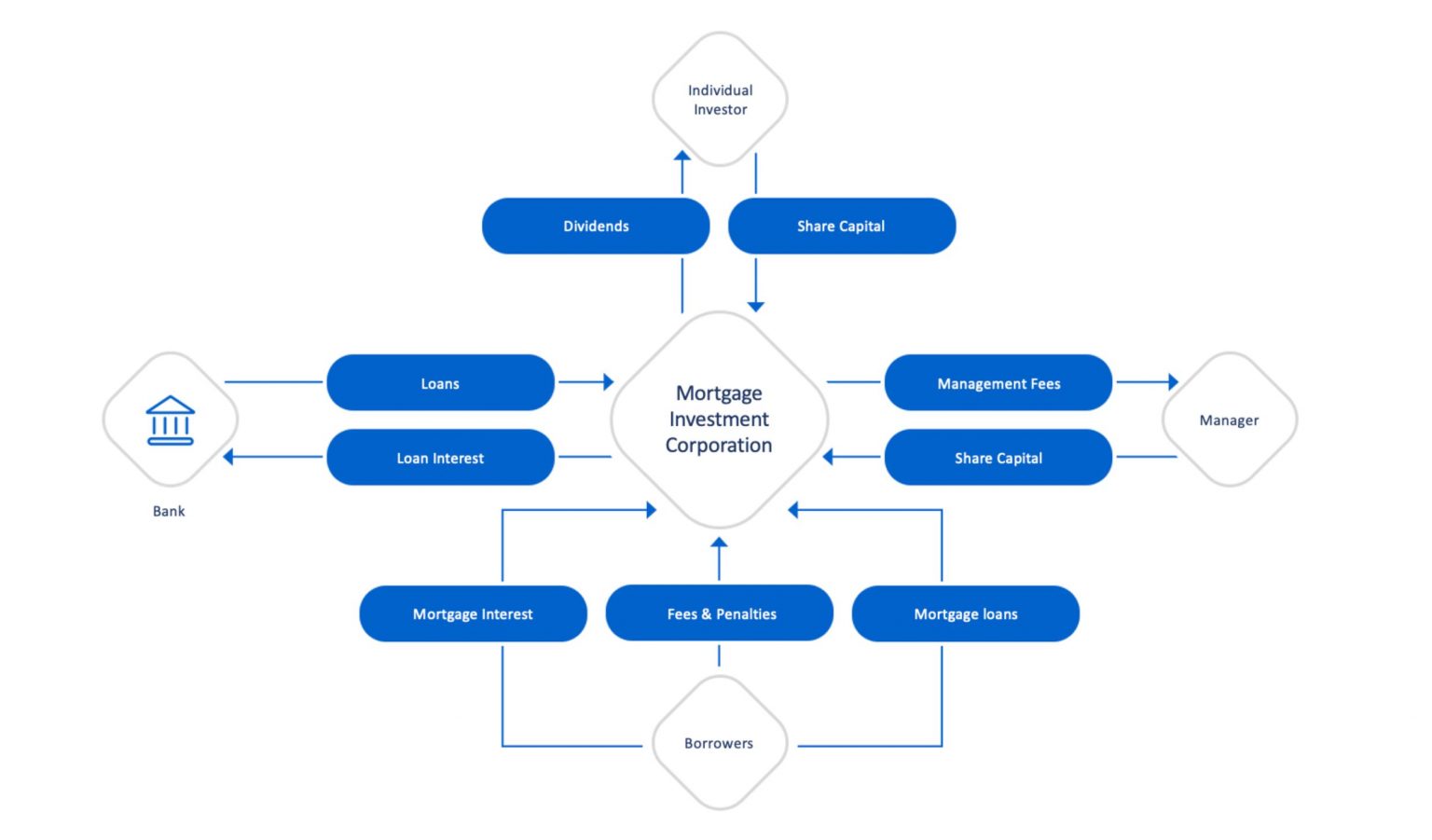

Just How MICs Source and Adjudicate Loans and What Occurs When There Is a Default Home mortgage Investment Corporations provide investors with straight exposure to the actual estate market with a pool of thoroughly selected home loans. A MIC is in charge of all elements of the mortgage investing procedure, from origination to adjudication, consisting of day-to-day administration.

CMI MIC Finances' strenuous credentials procedure allows us to handle home loan high quality at the really start of the financial investment process, lessening the possibility for repayment concerns within the finance profile over the term of each home loan. Still, returned and late payments can not be proactively taken care of 100 per cent of the moment.

We purchase mortgage markets across the country, allowing us to lend anywhere in Canada. To find out even more regarding our financial investment procedure, call us today. Call us by submitting the form below to learn more regarding our MIC funds.

Mortgage Investment Corporation - The Facts

At Amur Capital, we intend to provide a genuinely varied technique to alternate investments that take full advantage of return and capital preservation. By offering a series of traditional, earnings, and high-yield funds, we deal with a variety of investing purposes and choices that fit the demands of every individual investor. By purchasing and holding shares in the MIC, investors gain a proportional possession passion in the business and get income via reward payments.

In addition, 100% of the financier's capital obtains positioned in the selected MIC without ahead of time deal charges or trailer charges - Mortgage Investment Corporation. Amur Capital is concentrated on offering financiers at any type of degree with accessibility to professionally managed exclusive financial investment funds. Financial investment in our fund offerings is available to Alberta, British Columbia, Manitoba, Nova Scotia, and Saskatchewan residents and need to be made on a private positioning basis

Investing in MICs is a wonderful method to get exposure to Canada's successful property market without the demands of energetic home monitoring. Besides this, there are numerous other factors why capitalists think about MICs in Canada: For those seeking returns comparable to the securities market without the associated volatility, MICs offer a safeguarded actual estate financial investment that's less complex and may see this page be much more lucrative.

Actually, our MIC funds have actually historically delivered 6%-14% annual returns. * MIC financiers receive rewards from the rate of interest payments made by consumers to the home mortgage loan provider, forming a consistent passive income stream at greater rates than standard fixed-income safeties like government bonds and GICs. They can likewise select to reinvest the returns right into the fund for worsened returns.

The Definitive Guide for Mortgage Investment Corporation

MICs presently account for roughly 1% of the total Canadian home loan market and stand for an expanding Continued section of non-bank financial firms. As investor need for MICs expands, it is essential to comprehend how they function and what makes them different from traditional realty financial investments. MICs purchase mortgages, not actual estate, and consequently provide direct exposure to the real estate market without the included danger of building possession or title transfer.

normally between six and 24 months) (Mortgage Investment Corporation). In return, the MIC collects passion and charges from the consumers, which are then dispersed to the fund's favored shareholders as reward payments, typically on a month-to-month check basis. Due to the fact that MICs are not bound by much of the very same strict loaning needs as standard banks, they can set their very own standards for accepting financings

Mortgage Investment Corporations additionally enjoy unique tax obligation therapy under the Revenue Tax Obligation Act as a "flow-through" investment vehicle. To prevent paying income tax obligations, a MIC needs to disperse 100% of its internet revenue to shareholders.

The 30-Second Trick For Mortgage Investment Corporation

In the years where bond yields continuously declined, Mortgage Investment Companies and various other alternate assets grew in appeal. Yields have actually rebounded because 2021 as reserve banks have raised passion prices yet genuine returns stay unfavorable loved one to rising cost of living. Comparative, the CMI MIC Balanced Home loan Fund generated an internet annual yield of 8.57% in 2022, not unlike its performance in 2021 (8.39%) and 2020 (8.43%).

MICs provide financiers with a way to spend in the real estate market without in fact owning physical home. Instead, investors merge their money with each other, and the MIC uses that cash to money home mortgages for borrowers.

The Only Guide for Mortgage Investment Corporation

That is why we desire to assist you make an enlightened choice about whether. There are many benefits related to buying MICs, consisting of: Considering that financiers' cash is pooled with each other and invested across numerous residential or commercial properties, their portfolios are branched out throughout various realty types and customers. By owning a profile of mortgages, investors can minimize danger and prevent placing all their eggs in one basket.